Wait at least 60-90 days from getting your original loan to refinance. It typically takes this long for the title on your vehicle to transfer properly, a process that will need to be completed before any lender will consider your application. Refinancing this early typically only works out for those with great credit.

How soon can you refinance a car after buying it?

Wait at least 60-90 days from getting your original loan to refinance. It typically takes this long for the title on your vehicle to transfer properly, a process that will need to be completed before any lender will consider your application. Refinancing this early typically only works out for those with great credit.

Can I refinance twice in a year?

There’s no legal limit on the number of times you can refinance your home loan. However, mortgage lenders do have a few mortgage refinance requirements that need to be met each time you apply, and there are some special considerations to note if you want a cash-out refinance.

Can I refinance my car early?

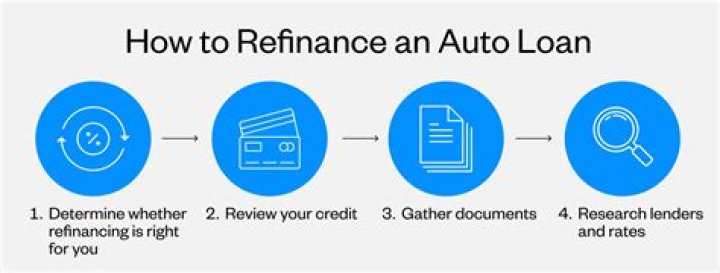

Strictly speaking, you can refinance your auto loan as soon as you find a lender that will approve the new loan. That may be a challenge since most lenders won’t refinance until the original car loan has been open for at least two to three months.Is refinancing a car worth it?

Refinancing can save you money in interest or stretch out your loan payments, but you should only consider it when the circumstances are right. If interest rates are lower or your financial situation has improved, it may be worth shopping around for a loan with better terms.

Can I refinance my car with the same lender?

The Takeaway It is generally possible to refinance your auto loan with your current lender. It may even be a bit easier than filling out an application with a new lender. But it doesn’t mean that it’s financially the best option for you.

Will refinancing my car lower my payment?

Refinancing and extending your loan term can lower your payments and keep more money in your pocket each month — but you may pay more in interest in the long run. On the other hand, refinancing to a lower interest rate at the same or shorter term as you have now will help you pay less overall.

How soon is too soon to refinance?

You’re required to wait at least seven months before refinancing — long enough to make six monthly payments. Any mortgage payments due in the last six months must have been paid on time, and you can have a maximum of one late payment (30 or more days late) in the six months before that.Is 3.125 a good rate?

Throughout the first half of 2021, the best mortgage rates have been in the high–2% range. And a ‘good’ mortgage rate has been around 3% to 3.25%.

Does refinancing hurt credit?Taking on new debt typically causes your credit score to dip, but because refinancing replaces an existing loan with another of roughly the same amount, its impact on your credit score is minimal.

Article first time published onWhat is a good interest rate on used cars?

Although there’s always going to be some wiggle room, the average used car loan interest rates are as follows: Excellent Credit (750 or Higher) – 5.1% APR. Good Credit (700 to 749) – 4.91% APR. Average Credit (600 to 699) – 5.89% APR.

Can I refinance my 2012 car?

Can you refinance an auto loan with an older car? Yes – but only up until a certain age. Most lenders won’t refinance a vehicle that is older than 10 years old or greater than 140,000 miles. Some lenders have even newer requirements, with lower mileage restrictions.

Is it cheaper to refinance with the same bank?

Closing costs on a refinance with the same lender You could see lower closing fees, though, if you refinance with the same lender, according to Barry Zigas, a senior fellow and former housing policy director with the Consumer Federation of America (CFA).

How do I renegotiate my car loan interest rate?

- Check your credit reports and build credit. …

- Apply for refinancing. …

- Apply with a co-borrower or add a cosigner. …

- Shop around. …

- Think about shorter loan terms. …

- Negotiate APR and interest rate. …

- See if you can lower your APR in just a few minutes.

Can a dealership refinance my car?

Myth: I just purchased my vehicle and the dealer said I can’t refinance for 6 months. Fact: The truth is, dealers are incentivized to keep you in your original loan. … If you love the car you found, but are unhappy with the interest rate and loan you received, you can apply to refinance at any time.

Are interest rates going up in 2021?

After mortgage rates hit an all-time low in January of this year, they quickly increased and have since dropped back down closer to their record lows. But many experts forecast that rates will rise by the end of 2021. As the economy begins to reopen, the expectation is for mortgage and refinance rates to grow.

What is a good interest rate for 84 month car loan?

LenderLowest RateTermsPenFed Credit Union Best Overall0.99%36 to 84 monthsLightStream Best Online Auto Loan2.49%24 to 84 monthsBank of America Best Bank for Auto Loans2.14%12 to 75 monthsConsumers Credit Union Best Credit Union for Auto Loans2.24%0 to 84 months

Is 3.625 a good rate?

Even with the latest increase, rates are largely still below 4% and considered to be historically low. If you’re interested in buying a home or refinancing a home loan, you should still be able to take advantage of favorable rates. The latest rate on a 30-year fixed-rate mortgage is 3.625%.

Is it bad to refinance after 6 months?

Your current lender might ask you to wait six months between loans, but you’re free to simply refinance with a different lender instead. However, you must wait six months after your most recent closing (usually 180 days) to refinance if you’re taking cash–out.

Does refinancing lower interest rate?

Refinancing can lower your monthly mortgage payment by reducing your interest rate or increasing your loan term. Refinancing also can lower your long-run interest costs through a lower mortgage rate, shorter loan term or both.

Does refinancing save money in the long run?

If you can recover your costs in two or three years, and you plan to stay in your home longer, refinancing could save you a bundle over time. … If you get a new 30-year mortgage several years into your original mortgage, you’re essentially lengthening the term of your loan, and that can cost you plenty.

Does transferring a car loan affect credit score?

Transferring a car loan can affect your credit score—even if you’re not behind on payments. When you transfer a loan, you effectively close an account, which could affect your credit age and your credit mix. In that case, you may see a temporary drop in your credit score.

Does refinancing affect taxes?

Mortgage interest and itemizing deductions Something to keep in mind is that refinancing your mortgage can significantly reduce your total tax deductions. Refinancing to a lower mortgage rate means you’ll be paying less interest, which means you’ll have less mortgage interest to deduct when tax time comes around.

Why did my credit score drop 40 points?

Pulling your credit report is the first step to identifying why your score dropped 40 points. You can identify all recent negative items that may have affected your score, leading to the drop. Remember that the most common reason for a 40 point drop is due to balance changes. … An old credit card account closed.

Is a 72 month car loan bad?

Generally, yes, a 72 month car loan is bad. When you get a 72 month car loan, you’re more likely to go upside down on your car loan, which leaves you in a vulnerable financial position. Avoid getting a 72 month car loan if you can. This might mean getting a cheaper car than you hoped for.

What is considered a high car payment?

According to experts, a car payment is too high if the car payment is more than 30% of your total income. Remember, the car payment isn’t your only car expense! Make sure to consider fuel and maintenance expenses. Make sure your car payment does not exceed 15%-20% of your total income.

What is the average interest rate on a car loan with a 750 credit score?

What is the average interest on a car loan with a 750 credit score? For a 750 credit score, the average auto loan rate is about 3.48 percent for new cars and 5.49 percent for used cars. Both of these rates are very good compared to the available range.

Can you refinance a car over 100 000 miles?

– Like age restrictions, lenders also have mileage requirements for refinancing. Vehicles with over 100,000 miles are typically going to be ineligible to refinance. Some lenders have higher mileage thresholds, although many also have lower mileage limits.

Can I finance a high mileage car?

Yes. Some banks will finance vehicles with high mileage because they understand that vehicles last longer than they used to. A private party auto loan, where you’re buying a car directly from the owner, may typically only be available to credit union members or bank customers.

What is the oldest car you can finance?

Typically, a bank won’t finance any vehicle older than 10 years, even if you have good credit. If you don’t have great credit, you may find it difficult to finance through a bank, even for a new car.

Why do lenders want you to refinance?

Your servicer wants to refinance your mortgage for two reasons: 1) to make money; and 2) to avoid you leaving their servicing portfolio for another lender. Some servicers will offer lower interest rates to entice their existing customers to refinance with them, just as you might expect.