Section 1245 is a way for the IRS to recapture allowable or allowed depreciation or amortization the taxpayer has taken on 1231 property. This recapture occurs at the time a business sells certain tangible or intangible personal property at a gain.

Is 1245 a capital gain?

To see how this would work in real time, here is a basic example of the tax treatment of a Section 1245 property gain. … Of the total gain amount, $7,142.85 (the amount you’ve taken in depreciation) would be taxed as ordinary income, and the remaining $500 would be taxed as long-term capital gains.

How is 1245 depreciation recapture calculated?

Section 1245 recapture is computed as the lesser of: (1) allowable depreciation or amortization on the disposed assets, or (2) the gain realized upon the disposition.

Is a 1250 gain a capital gain?

Since the unrecaptured section 1250 gains are considered a form of capital gains, they can be offset by capital losses.How is 1245 gain taxed?

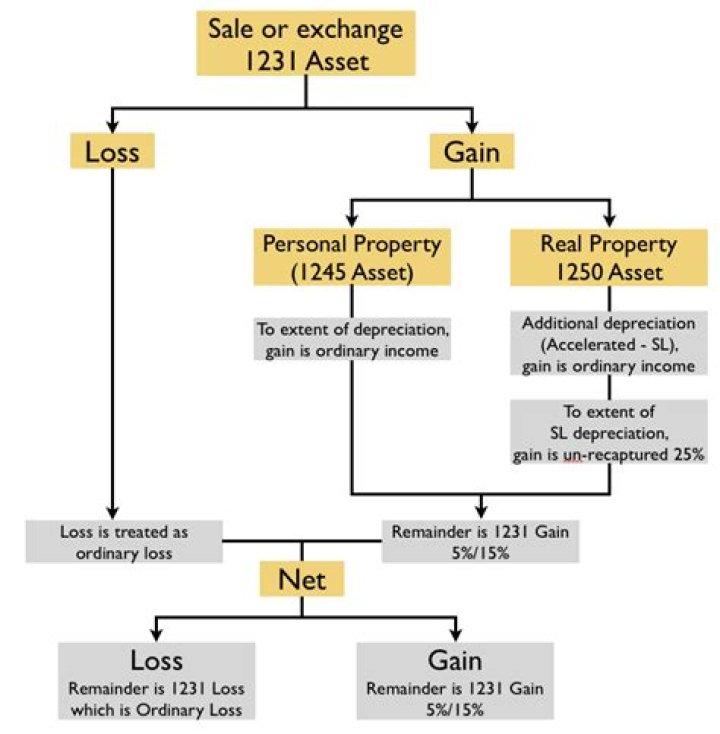

Sections 1245 and 1250 serve as “recharacterization” provisions, meaning Section 1231 assets which meet the definition of either may potentially have all or a portion or gain from their disposition recharacterized as either ordinary income or capital gain taxed at 25 percent.

What are 1231 gains?

Understanding Section 1231 Gains Section 1231 gains are gains from depreciable property and real property used in a trade or business and held for more than one year, other than inventory or property held for sale in ordinary course. Such gains have traditionally enjoyed “favored nation” status in the Code.

How is section 1245 gain reported?

The gain treated as ordinary income by §1245 is the amount by which the lower of the property’s (1) amount realized or fair market value (depending on the type of disposition), or (2) recomputed basis (i.e., the property’s basis plus all amounts allowed for depreciation) exceeds the property’s adjusted basis.

Why does 1250 recapture generally no longer apply?

Why does §1250 recapture generally no longer apply? … §1245 recapture trumps §1250 recapture. Because unrecaptured §1250 gains now apply to all taxpayers instead. The Tax Reform Act of 1986 changed the depreciation of real property to the straight-line method.What is the capital gains tax rate for 2021?

For example, in 2021, individual filers won’t pay any capital gains tax if their total taxable income is $40,400 or below. However, they’ll pay 15 percent on capital gains if their income is $40,401 to $445,850. Above that income level, the rate jumps to 20 percent.

What happens when you sell a fully depreciated asset?Selling Depreciated Assets When you sell a depreciated asset, any profit relative to the item’s depreciated price is a capital gain. … If you used the Section 179 deduction, for example, to write down the cost of the computer to nothing and sold it for $1,200, the entire selling price would be a taxable gain.

Article first time published onCan you avoid capital gains tax by investing in real estate?

When you sell a rental or investment property, you can roll the proceeds of the sale into a similar type of investment to avoid CGT. This is called a 1031 exchange and it is popular among real estate investors as a strategy for building wealth.

What does recapture mean in real estate?

Recapture allows a seller of some asset or property to reclaim some or all of it at a later date. The seller will have the option to buy back what has been sold, within a certain window of time, often at a higher price than what it was initially sold for.

Can you write off loss on sale of land?

The IRS allows you to use up to $25,000 of passive activity losses, like your loss on your investment land, to offset other income. The drawback to this provision is that you can only claim the full offset if your adjusted gross income is $100,000 or less.

Is Goodwill a 1245 property?

Section 1245 Property is any new or used tangible or intangible personal property that has been or could have been subject to depreciation or amortization. Goodwill and the covenant not to compete are Section 1245 property as they are intangible property subject to amortization.

Are computers section 1245 property?

Section 1245 property does include personal property. Assets such as computers, desks, chairs, copiers, etc. are all personal property falling under Section 1245.

What is the capital gain tax for 2020?

Capital Gains Tax RateTaxable Income (Single)Taxable Income (Married Filing Separate)0%Up to $40,000Up to $40,00015%$40,001 to $441,450$40,001 to $248,30020%Over $441,450Over $248,300

How do I avoid capital gains tax on commercial property?

- deducting capital losses.

- long-term investments.

- qualified opportunity zones.

- 1031 Tax-deferred exchange.

- 1033 Tax-deferred exchange.

- 721 Tax-deferred exchange.

- Section 453: Installment Sale Tax Deferral.

When a result results the sale of section 1245 property?

When a gain results from the sale of Section 1245 property, how does the taxpayer determine the amount that should be taxed as ordinary income? The lesser of the recognized gain or the accumulated depreciation on the asset is ordinary income. The current year’s depreciation is recaptured as ordinary income.

What type of property is 1231?

Section 1231 property is real or depreciable business property held for more than one year. A section 1231 gain from the sale of a property is taxed at the lower capital gains tax rate versus the rate for ordinary income. If the sold property was held for less than one year, the 1231 gain does not apply.

What constitutes capital gains?

Key Takeaways. A capital gain occurs when you sell an asset for more than you paid for it. If you hold an investment for more than a year before selling, your profit is typically considered a long-term gain and is taxed at a lower rate.

Is Goodwill a capital asset?

Goodwill is an intangible asset, but also a capital asset. The value of goodwill refers to the amount over book value that one company pays when acquiring another. Goodwill is classified as a capital asset because it provides an ongoing revenue generation benefit for a period that extends beyond one year.

How long do you have to live in a house to avoid capital gains tax?

Live in the house for at least two years. The two years don’t need to be consecutive, but house-flippers should beware. If you sell a house that you didn’t live in for at least two years, the gains can be taxable.

Is Social Security taxable?

Some of you have to pay federal income taxes on your Social Security benefits. between $25,000 and $34,000, you may have to pay income tax on up to 50 percent of your benefits. … more than $34,000, up to 85 percent of your benefits may be taxable.

What are the 7 tax brackets?

There are seven tax brackets for most ordinary income for the 2021 tax year: 10%, 12%, 22%, 24%, 32%, 35% and 37%. Your tax bracket depends on your taxable income and your filing status: single, married filing jointly or qualifying widow(er), married filing separately and head of household.

What is the Section 1245 recapture rule?

Section 1245 recaptures depreciation or amortization allowed or allowable on tangible and intangible personal property at the time a business sells such property at a gain. Section 1245 taxes the gain at ordinary income rates to the extent of its allowable or allowed depreciation or amortization.

Where does unrecaptured 1250 gain go on 1040?

Report your share of this unrecaptured gain on the Unrecaptured Section 1250 Gain Worksheet – Line 19 in the Instructions for Schedule D (Form 1040) as follows. Report unrecaptured section 1250 gain from the sale or exchange of the partnership’s business assets on line 5.

What does it mean to characterize a gain or loss why is characterizing a gain or loss important?

Characterizing the gain or loss is important because the tax treatment for gains and losses vary depending on the character. Ordinary gains and losses are taxed at ordinary income rates, regardless of the holding period.

Can you depreciate an asset to zero?

Every asset has a useful life, which is an accounting estimate of how long that asset will last. … This continues until the asset is fully depreciated. Assets get depreciated down to zero or to their salvage value, which is what the company thinks it could get for the asset at the end of its useful life.

What happens when NBV is zero?

At the end of the asset’s tax recovery period (useful life), the asset will be fully depreciated and the NBV will be zero. Accordingly, there will no longer be a depreciation tax benefit to the taxpayer going forward.

Does selling equipment count as income?

Business equipment, including vehicles and machinery, is considered an asset, even after it depreciates. Like all capital gains and losses, you report the income or loss from the sale of the equipment on IRS Form 1040.

Do seniors pay capital gains tax?

Today, anyone over the age of 55 does have to pay capital gains taxes on their home and other property sales. There are no remaining age-related capital gains exemptions. However, there are other capital gains exemptions that those over the age of 55 may qualify for.